Two years ago, the board at Hide Lake School District hired Superintendent Mona Henderson to steer the district out of a budget deficit. Henderson introduced strict budgeting protocols, taking full control of the process and presenting recommendations for board approval. The board typically accepted her proposals with minimal discussion, believing this approach would avoid past financial missteps.

However, a newly elected board member raised concerns, questioning whether the board was relinquishing its obligation to oversee the district’s finances. She argued that rubber-stamping the superintendent’s decisions without deeper engagement might compromise their role as stewards of the district’s financial health. The board president responded cautiously, recalling how a lack of financial expertise among board members had contributed to previous challenges.

This scenario underscores a key point: while administrators like superintendents and their teams bring valuable expertise, the financial stewardship of public entities is a shared responsibility. Governing board members must actively participate in financial oversight, working in partnership with professionals to ensure sound decision-making.

The balance between trusting expert advice and fulfilling fiduciary responsibilities is essential for maintaining the financial health of the organizations they serve.

However, school board members and other elected or appointed governance boards are, for the most part, lay people. They come from different professions and backgrounds – their diversity represents their communities and their interest. Budgeting and other financial management may or may not be among their skill sets.

A recent study of school board financial deliberations by Georgetown University’s Edunomics Lab revealed that many district budget decisions were on autopilot. Many board members did not ask questions.

“In 71% of meetings, various financial decisions were approved via consent agenda (which involves approval of numerous items bundled under a single vote with no discussion, typically done for expediency) and some budgetary items were placed on the consent agenda,” according to the study.

Governing boards must understand how their budget works, as well as how to budget strategically to meet their goals. Without this understanding and oversight, board members could miss spending that may be working against the organizations’ overall goals. Worse, they may be overlooking waste or even fraud in the district or organization.

As Dr Chad Bledsoe, President of Montgomery Community College points out,

"The term financial oversight and, by default, risk oversight talks to the idea of governance to ensure that the institution is maintaining fiscal responsibility, that the resources are going where they're supposed to, and that we're meeting the needs of the community by default our programs. The board has the responsibility of ensuring that the institution is meeting its mission, i.e. serving the educational needs of the community. And that can't be done if there is not adequate oversight of financial resources."

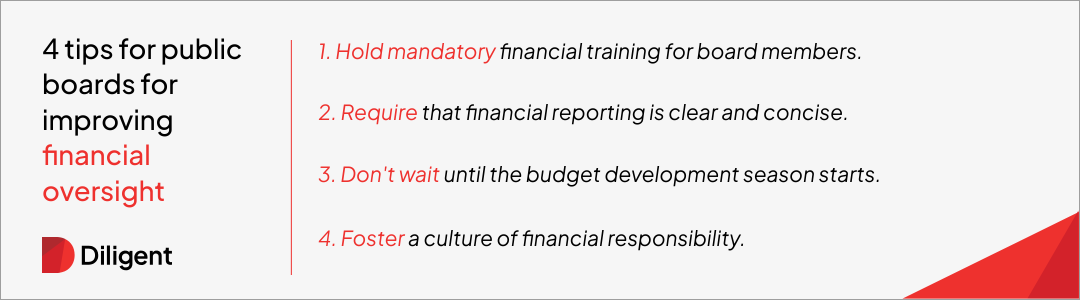

District or organization staff should use accurate accounting practices. It’s the board’s responsibility to regularly review financial reports, and members should be able to ask knowledgeable questions.

Frequent financial reports assist board members in addressing issues while problems are still small. The financial reports should be comprehensive and easy to understand.

At the minimum, board directors should become proficient at reading these essential financial statements: the balance sheet, the income statement and the cash flow statement.

Here are four simple ways to strengthen your board’s ability to oversee finances:

All boards have a code of ethics that describes and promotes ethical behavior among board members. Board directors must emulate the culture in word and deed.

Many boards don’t spend enough time promoting an ethical culture, even though they agree that culture is a key driver of ethical behavior. This is especially true when it comes to accurate financial reporting. Some boards schedule dedicated time at meetings or retreats to focus on developing an ethical board culture.

While board members are willing to accept the challenge of overseeing ethics and compliance matters, they're often unsure about what questions to ask and what information they should be looking for.

Developing strategies for ethical behavior and communicating them is a skill they can develop along with an understanding of finances. Many directors need additional training on culture and risk management.

A red flag may be nothing more than an issue that makes a board director uncomfortable, or that doesn't sit well with them. They should be quick to act on past, present or potential areas of fraud.

Addressing issues of ethics is a sensitive area and one that makes people uncomfortable. It's best to deal with issues up front rather than risk a more serious situation down the line.

Ethics and compliance don’t have to feel overwhelming. In our guide we break it all down: why ethics oversight matters plus steps to building stronger governance strategy.

Budgeting and finances can be difficult to tackle, especially for new board members. Diligent Community offers several robust features that can significantly enhance financial oversight for publicly elected boards.

Find out how Diligent Community can help your board by requesting a demo.